Download Your Free Guide Now!

Did you know that you might need to divorce your spouse AND your mortgage?

Most people don’t.

That’s why we’ve created this popular guide which pulls back the curtain on everything you need to know, and need to consider, before you’re truly ready to divorce your mortgage.

Top 8 Mortgage Misconceptions

1. I’m better off working with my bank. They’ve known me for years.

Don’t expect preferential treatment just because you have a prior banking relationship. You need to meet their requirements to get approved. By limiting yourself to just one lender, you’re at the mercy of their rates, their guidelines, and their loan products. The benefit to working with a broker is simple – you have options.

2. All mortgage lenders have the same rules and requirements.

Every lender has their own unique set of guidelines. These guidelines also vary based on loan amount, credit score, and property type (primary, investment, etc.).

3. Mortgage rates are too high. I don’t want to refinance.

While rates have increased slightly, they remain at near historic lows. Also, consider whether your payment is fixed for the entire period. If not, you could face significantly higher payments in the future.

4. I’m still on a joint mortgage with my former spouse. I’m worried those payments will count against me when I apply for a new mortgage.

Verbiage matters. If the Marital Settlement Agreement (MSA) specifies that your spouse is solely responsible for the payments, a new lender will not debt service you for said payments (i.e., they won’t count against you).

5. I signed an Interspousal Transfer Deed and came off title – I’m finally free from the house.

Coming off title and coming off the mortgage are two different things. If your name is still on the mortgage, your credit is at risk. The only way to come off the mortgage is for your spouse to refinance or pay off the loan.

6. I’m receiving spousal and child support. That will help me qualify.

Generally speaking, child and spousal support require a 6-month history of receipt and 3 years continuance from the date of your loan application.

7. I have a high income – getting a loan should be easy.

Not all income is considered ‘qualified’ income from a lenders perspective. For example, cash bonuses typically require a 2-year history and stock options are rarely considered.

8. I have significant liquid assets. That makes me a strong borrower.

Qualifying depends primarily on your debt-to-income (DTI) and loan-to-value ratios (LTV). Unfortunately, lenders don’t weigh liquid assets heavily in determining whether you qualify.

Divorce Mortgage vs. Standard Mortgage: How They Differ

Not all mortgages are created equal. Here’s what sets them apart.

Top 5 Reasons to Refinance in Divorce

1. Protect your credit. If your spouse is buying you out of the family residence, you’re not off the hook. If you’re still on the mortgage, then you’re at risk. Late payments could destroy your credit. The only way to truly protect yourself is for your spouse to refinance. If at all possible, the Marital Settlement Agreement should require the spouse keeping the house to refinance shortly after the divorce (and include provisions to address what happens in the event the spouse doesn’t follow through).

2. Buy out your spouse. A cash-out refinance is an often-overlooked strategy for coming up with funds to buy out your spouse’s interest in the house. The purpose of a cash-out refinance is to tap into the equity from your home by taking a new mortgage that is bigger than the existing mortgage.

3. Tap into your home equity. Coming up with buyout funds is not the only reason to consider a cash-out refinance. The equity in your house can be a great source of liquidity. Some of the most common reasons to tap into your home equity include debt consolidation (paying off high-interest credit cards, HELOCs, and other loans), establishing a cash reserve (emergency fund), home improvements, or paying attorney fees.

4. Lock in fixed mortgage payments. Do you have an adjustable rate mortgage (ARM)? If so, it’s important to understand how rising rates would impact future payments. To mitigate the risk of rising rates, consider refinancing to a fixed-rate mortgage (or even an ARM with a longer fixed period).

5. Lower your mortgage payment. With the extra expense that comes with supporting two households, it’s critical to find ways to improve your cash flow. By refinancing, you may be able to lower your monthly payment (by lowering your rate, switching to a different loan product, or spreading your payments over a longer time frame).

You can read the full article at Forbes.com.

The 3 Loan Buckets: An Overview

Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs) which purchase conforming loans from lenders. By selling loans to Fannie and Freddie, lenders gain access to funds for future loans.

Jumbo Loans are not eligible to be purchased by Fannie and Freddie. As a result, lenders either sell jumbo loans to private investors or keep them as an investment.

What guidelines matter most?

• Debt-to-income (DTI) ratio: Lenders want to ensure that you can repay your mortgage. If your monthly debts exceed a certain percentage of your monthly income, you won’t qualify.

• Loan-to-value (LTV) ratio: As simple as it sounds. Take your loan amount and divide it by your property value. The lower the LTV, the better.

• Credit (FICO) score: There are three credit bureaus that issue credit scores (Equifax, Transunion, Experian). Lenders use the middle score to assess your creditworthiness.

Loan Products: Defined

At Divorce Mortgage Advisors, we like to keep things simple.

You want the best mortgage rate, and part of getting that will be understanding a few basics. With that in mind, here is a summary of the loan products available to you along with some relevant definitions:

Adjustable Rate Mortgage (ARM) Products

The following ARMS have a 30-year term.

- 3/1 ARM - The rate is “fixed” for the first 3 years, and then becomes variable for the next 27 years based on an index rate plus a margin.

- 5/1 ARM - The rate is fixed for the 1st 5 years, and then becomes variable for the next 25 years based on your index plus a margin.

- 7/1 ARM - The rate is fixed for the 1st 7 years, and then becomes variable for the next 23 years based on your index plus a margin.

- 10/1 ARM - The rate is fixed for the 1st 10 years, and then becomes variable for the next 20 years based on your index plus a margin.

Fixed Rate Mortgage Products

- 10-year fixed – Paid over 10 years, fixed payments for all 10 years.

- 15-year fixed – Paid over 15 years, fixed for all 15 years.

- 20-year fixed – Paid over 20 years, fixed for all 20 years.

- 30-year fixed – Paid over 30 years, fixed for all 30 years.

Pro Tip: As a rule of thumb, the longer the fixed period, the higher the interest rate.

Wait, there’s more!

Here are some specialty loan products and strategies to be aware of.

- Cross-collateral. Do you need the sale proceeds from your current house to come up with the down payment for your new house? That’s where a cross-collateral loan comes into play.

- Departing residence. If you’re buying a new house and converting your primary residence to a rental property, you may be able to get credit for potential rental income. Some lenders will allow for a ‘fair market rent survey’ to determine the rental income credit.

- Reverse mortgage. A reverse mortgage, also known as a Home Equity Conversion Mortgage (HECM), allows you to use a portion of the equity in your home to pay off your existing mortgage. You can then use the remaining proceeds however you like. The loan payments can be deferred for as long as you occupy the property. Keep in mind you are still responsible for paying property taxes and homeowners insurance. There are a number of eligibility requirements. For instance, you must be at least 62 years of age.

- 40-year term. A jumbo loan paid over 40 years. Since the payments are spread over a longer period, the payments are typically lower than a 30-year term which enables a borrower to qualify for a higher loan amount. 40-year terms typically carry higher rates than 30-year term.

We’ve really just scratched the surface here. Don’t hesitate to contact us for details.

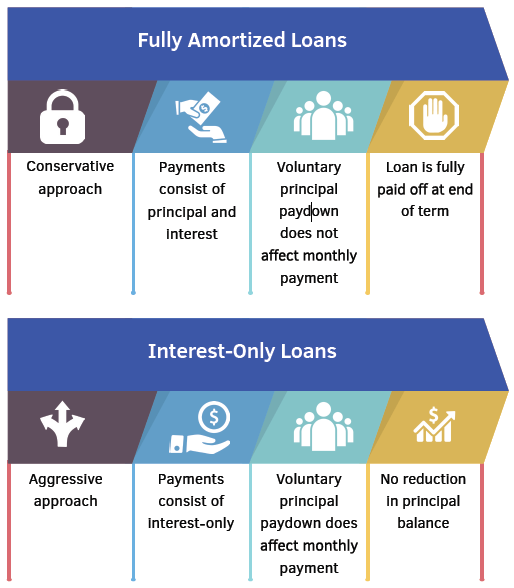

Fully Amortized vs. Interest-Only Loans

Risk alert: Once the interest only period expires, you have a shorter period to pay off the remaining principal balance. If you don’t refinance, your monthly payments will increase dramatically.

HELOCs: Another Option

A home equity line of credit (HELOC) is just that — a line of credit. Think of a HELOC like you would a credit card: You use it to make purchases, and then pay for those purchases later.

Unlike a credit card, which is unsecured debt, a HELOC is secured because it’s backed by an asset with value: your house. When you make your mortgage payment each month, and as the market value of your home goes up, you’re building equity. A HELOC allows you to borrow against that equity.

Once you’ve been approved for a HELOC, you can borrow as much or as little as you need. This is what sets a HELOC apart from a home equity loan, in which the bank lends you a lump sum. With a HELOC, you don’t borrow it until you need it.

Most HELOCs have variable interest rates, which means they go up and down based on a financial index, typically the prime rate. Some banks will add a few percentage points, called a margin, to the prime rate.

You can use a HELOC for many reasons, including but not limited to:

- Attorney Fees

- Equalizing Payments

- Emergency Funds

- Home Improvement

- Debt Consolidation

The Loan Process: Start to Finish

Here are 9 critical steps for you to understand to help ensure a smooth and successful loan closing.

Step 1 – Think Ahead

By failing to prepare, you are preparing to fail. Preparation makes all the difference between a seamless closing and a stressful one. Start by having your mortgage advisor run a credit report to confirm your FICO, check your debts, and clear up any delinquencies or inaccuracies.

In addition, you will likely receive a checklist of required documentation. Gather the documents in this list ASAP. There’s no avoiding it. The more information your lender has to work with up-front, the easier the process will be for all parties involved.

Step 2 – Choose the Right Loan for You

To determine which loan is right for you, ask yourself the following questions:

- What is the purpose of the new loan? (remove spouse, buyout, etc.)

- What do you hope to achieve with a refinance? (save monthly, pay it off faster? etc.)

- How long do you expect to own this property?

- Are you familiar with the different loan products available today?

- What is your risk tolerance for rate and/or payment adjustments on your new loan?

If you aren’t sure – ASK. Your mortgage advisor’s primary responsibility is making sure that the loan product and terms you select are in line with your goals and needs.

Step 3 – Lock your mortgage rate

Once you are satisfied with your loan terms, you're ready to lock your rate.

A rate lock is important because it protects you from rising yields. An unlocked loan is considered a ‘floating’ loan, and this approach is highly risky because your rate will continue to fluctuate daily. This is akin to gambling.

Rate locks are for a specific period of time (typically 30-45 days). In general, the longer your rate is locked - the higher the associated cost. Generally speaking, most loans close between 30-45 days depending on the lender.

You will likely need to sign lender specific disclosure at this point as well. Be sure to review these disclosures and confirm accurate terms and closing costs.

Step 4 – Order home appraisal

The reality about appraisals is that every loan needs one. In fact, every lender needs their own appraisal report generated from their own appraisal management company. These reports are not transferrable between lenders, so be sure to select the lender you want to apply with before paying for and proceeding with any appraisal orders.

Step 5 – Mortgage underwriting review

By this point, you’ve provided your mortgage advisor with all the necessary paperwork (see section on Document Requirements). Your completed loan application and appraisal will be forwarded to an underwriter to be reviewed. The underwriter is going to look carefully at each of the documents that you provided to determine your capacity to make the payment on this loan. They will also confirm that you meet all the credit guidelines as set forth. Be prepared to provide additional documentation or explanations after the underwriter's review.

Step 6 – Review Loan Approval and Conditions

If the underwriter is satisfied with your loan application, they will issue an approval letter and a list of approval conditions (yes, one last round of paperwork). Approval conditions are the final items needed in order to get your file ready for closing. Read through your approval letter carefully to make sure that the loan terms approved by the underwriter match what you thought you were getting. Also, review your conditions to make sure that you can satisfy all of the underwriter's requirements.

Step 7 – Clear To Close

Once your conditions are reviewed and accepted by the underwriter your mortgage advisor will order your Closing Disclosure. This final Closing Disclosure lists all expected closing costs and contains another overview of your loan terms. It is critically important to review the details carefully to ensure that there are no surprises at close. If you have questions about your preliminary closing statement, bring them to your advisors attention prior to sitting down at the closing table. If everything is good to go on the preliminary closing statement, you can select a formal signing date.

Step 8 – Signing

Finally, you are ready to sign your documents. Your mortgage advisor will confirm where and when the signing will occur. At the closing table, you will be asked for identification so make sure you bring a driver's license, state issued identification or passport. Most signings last anywhere between 30-90 minutes.

Step 9 – Fund and Record

If you are refinancing an owner-occupied residence, you will have a three day right-of-rescission period. If you decide to cancel, you need to contact your mortgage advisor prior to the expiration of the cancellation period.

After the cancellation period expires, your lender will fund your loan. Proceeds will disburse to pay off your existing loan (if you have one) and the escrow office will record your new mortgage and Deed of Trust with the County.

We hope this helps shed some light onto an otherwise unclear process. If you’re ever in doubt, ask for help. Your divorce mortgage advisor is your concierge.

What NOT To Do

Many people make decisions before and during the loan process that may jeopardize their loan approval. Here’s what not to do.

- Don’t change your job

- Don’t quit your job

- Don’t move your bank accounts without the green light

- Don’t buy anything you have to finance (cars, trucks, furniture, etc).

- Don’t open any new consumer credit accounts.

- Don’t be late on any of your credit liabilities or charge excessively.

- Don’t make large deposits into your bank accounts that you don’t want to explain or document.

- Don’t co-sign on a loan for anyone.

- Don’t fail to disclose any debts, obligations, or other pertinent information.

- Don’t spend savings budgeted for your down payment or cash needed at closing.

- Don’t forget to disclose child support or spousal support payments.

Remember, your loan is not final until it has funded and recorded.

“What-If” Analysis

There are several important stages to your divorce settlement process, and the initial stages are often the most critical. What you do early on in the process can set the table for success. Our job is to make sure you’re prepared.

There is one service that every divorcing individual should be sure to take advantage of when looking to refinance or purchase a new home:

Enter, the “what-if” analysis.

Of course, this will play a pivotal role in determining whether you can qualify.

But what makes the “what-if” analysis SO valuable is that it gives you a simple, foolproof way of evaluating how the variables in your divorce settlement (income, debts, etc.) can directly impact your ability to get a new loan.

This can help you answer the all-important question of how will spousal and/or child support affect your ability to qualify.

We all know that divorce is a moving target, with negotiations and settlement discussions unfolding over a period of months - sometimes years.

Our “what-if” analysis can quickly and easily be revised to reflect proposed changes to your settlement.

By obtaining a “what-if” analysis early in the game, you will notice how much easier it is to prepare for changes as they are presented to you.

Did You Know

- A minimum of 6 months history of receipt for spousal and/or child support is required

- Support needs minimum 3 years of continuance (i.e. can’t terminate within 3 years of loan closing). For example, if your child is 16 and child support terminates at age 18, none of it will count for income.

- Child support can be grossed up by 25% - providing you with additional qualifying income!

- With most payments and obligations, lenders enter this as a ‘debt’ when calculating your debt-to-income ratio. Spousal support is treated differently. It is entered as a reduction of income. Without getting overly technical – this substantially improves your ability to qualify.

- Your Marital Settlement Agreement (MSA) and judgment don’t necessarily need to be finalized. In some instances, your loan can be funded with a signed Memorandum of Understanding (MOU) or other simpler alternatives.

Financial and Divorce Documents Needed

Gathering documents can seem like a daunting task, but it doesn’t have to be—if you’re prepared.

Essential:

• Two years tax returns (personal and/or business)

• Two years W-2’s

• Two most recent pay stubs

• Current mortgage statements

• Two months of bank statements

• Explanations for any credit delinquencies

• Current homeowners insurance policies

Divorce-Specific:

• Marital Settlement Agreement (MSA) or judgment

• Evidence of spousal and/or child support payments received

This is far from an exhaustive list. Lenders frequently request additional documentation throughout the loan process.

Give us a call and we can provide a more detailed checklist tailored to your situation.

This way you’ll enjoy a seamless loan closing from start to finish.

FAQ

How do you charge?

Clients are often surprised to learn that they pay us nothing. We’re compensated by the lender—and our only incentive in selecting a lender is finding you the best terms possible.

What stage in the process do you get involved?

The earlier the better. Getting involved early enables us to offer guidance on how the mortgage fits into your settlement strategy—and we can always revisit the underwriting analysis as settlement negotiations unfold.

I’m planning to buy out my spouse. What should I be thinking about?

Your spouse will likely want to come off the mortgage which means you will be required to refinance. The first step is confirming that this is a viable option. We can help assess how property division and support proposals affect your ability to qualify.

My spouse is keeping the house. Do I still need to contact you?

Absolutely. Before you agree to a settlement, you should ensure ALL proposals are feasible. This includes confirming your spouse can qualify to refinance.

I am planning to buy a house down the road. What should I do to prepare?

Agreements reached today can impact your ability to qualify in the future. We can review the MSA for any potential pitfalls and provide insight on how a lender may interpret various provisions.

How does timing impact my financing options?

Timing is KEY. For instance, it’s not uncommon for an otherwise qualified borrower to approach us post-divorce only to learn that the support paid precludes them from qualifying.

How do I get started?

Simply get in touch with us, and we’ll supply you with a short list of the information we need to assess your mortgage proposal. Then, we’ll provide an in-depth analysis detailing how much you qualify for and the sensitivity to key variables (e.g., support, debt restructuring, etc.).

Congrats! If you’ve made it this far then you:

• Recognize what sets divorce mortgages apart

• Have a blueprint for the top reasons to refinance in divorce

• Know your options and loan types

• Understand the importance of a “what-if” analysis during divorce settlement negotiations

• Have a grasp on the financial documents you’ll need to gather

• Value the importance of working with a Divorce Mortgage Advisor